All Categories

Featured

Table of Contents

That typically makes them a much more cost effective option for life insurance coverage. Some term policies might not keep the premium and survivor benefit the very same with time. You do not wish to wrongly believe you're acquiring degree term coverage and after that have your death advantage change in the future. Many individuals obtain life insurance policy protection to assist monetarily protect their loved ones in instance of their unanticipated death.

Or you might have the choice to convert your existing term insurance coverage into an irreversible policy that lasts the rest of your life. Different life insurance policy plans have possible benefits and downsides, so it's crucial to comprehend each prior to you decide to purchase a policy.

As long as you pay the premium, your recipients will certainly receive the survivor benefit if you die while covered. That stated, it's essential to keep in mind that a lot of plans are contestable for 2 years which means protection might be rescinded on fatality, must a misstatement be discovered in the application. Plans that are not contestable typically have actually a graded death advantage.

Costs are usually lower than entire life policies. You're not locked into a contract for the rest of your life.

And you can't pay out your policy throughout its term, so you will not obtain any kind of economic gain from your past coverage. Similar to other kinds of life insurance coverage, the price of a degree term plan depends upon your age, protection needs, work, way of living and health. Typically, you'll discover extra economical coverage if you're younger, healthier and much less high-risk to insure.

Premium Guaranteed Issue Term Life Insurance

Because degree term costs remain the exact same for the duration of insurance coverage, you'll recognize precisely how much you'll pay each time. Level term coverage also has some versatility, allowing you to personalize your policy with added attributes.

You may need to satisfy certain problems and qualifications for your insurer to establish this rider. Furthermore, there might be a waiting period of as much as 6 months prior to working. There also can be an age or time limit on the insurance coverage. You can add a youngster rider to your life insurance coverage plan so it additionally covers your youngsters.

The survivor benefit is usually smaller, and coverage generally lasts till your kid transforms 18 or 25. This motorcyclist might be a more cost-efficient method to assist ensure your children are covered as motorcyclists can typically cover numerous dependents simultaneously. As soon as your child ages out of this protection, it might be possible to transform the cyclist right into a brand-new policy.

When contrasting term versus irreversible life insurance coverage. term life insurance with accelerated death benefit, it is essential to keep in mind there are a couple of various types. One of the most typical type of permanent life insurance policy is entire life insurance coverage, however it has some essential differences compared to level term protection. Right here's a basic overview of what to consider when contrasting term vs.

Entire life insurance policy lasts for life, while term protection lasts for a certain duration. The premiums for term life insurance policy are usually reduced than whole life protection. Nonetheless, with both, the costs remain the same for the duration of the policy. Entire life insurance coverage has a cash worth component, where a section of the premium might grow tax-deferred for future demands.

One of the main functions of level term protection is that your premiums and your death advantage don't change. You might have coverage that starts with a death advantage of $10,000, which can cover a home mortgage, and after that each year, the fatality advantage will decrease by a collection quantity or percentage.

Because of this, it's often a much more economical sort of degree term coverage. You might have life insurance policy with your company, however it might not suffice life insurance for your requirements. The first action when purchasing a policy is figuring out just how much life insurance policy you need. Take into consideration aspects such as: Age Family members dimension and ages Work standing Income Financial debt Way of living Expected final expenditures A life insurance calculator can aid identify just how much you need to start.

After determining on a plan, complete the application. For the underwriting procedure, you may need to provide basic individual, health and wellness, way of living and work info. Your insurer will certainly determine if you are insurable and the danger you may present to them, which is reflected in your premium costs. If you're approved, authorize the documents and pay your very first costs.

Outstanding Short Term Life Insurance

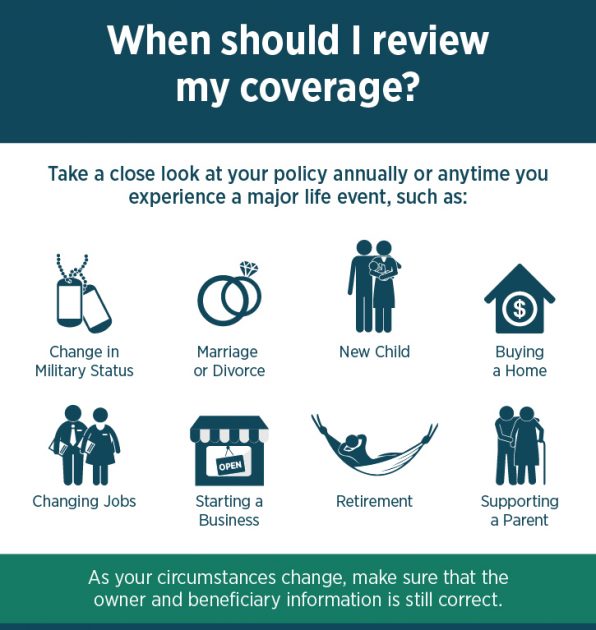

Think about organizing time each year to examine your plan. You might want to update your beneficiary details if you have actually had any kind of substantial life adjustments, such as a marital relationship, birth or separation. Life insurance policy can occasionally really feel complicated. You do not have to go it alone. As you explore your choices, consider discussing your demands, desires and concerns with an economic specialist.

No, level term life insurance coverage does not have cash money worth. Some life insurance coverage plans have an investment attribute that allows you to construct cash money value over time. A section of your premium payments is set aside and can earn interest gradually, which expands tax-deferred throughout the life of your insurance coverage.

You have some options if you still want some life insurance coverage. You can: If you're 65 and your insurance coverage has actually run out, for instance, you might desire to purchase a new 10-year level term life insurance coverage plan.

Tax-Free Level Term Life Insurance

You may have the ability to transform your term coverage right into an entire life plan that will last for the remainder of your life. Many types of level term plans are exchangeable. That means, at the end of your insurance coverage, you can convert some or every one of your plan to entire life insurance coverage.

Degree term life insurance policy is a plan that lasts a set term normally in between 10 and three decades and includes a level survivor benefit and level costs that remain the very same for the whole time the plan is in result. This means you'll know exactly just how much your repayments are and when you'll need to make them, allowing you to budget plan accordingly.

Level term can be a great choice if you're aiming to acquire life insurance policy protection for the very first time. According to LIMRA's 2023 Insurance coverage Measure Study, 30% of all grownups in the U.S. requirement life insurance policy and don't have any type of policy. Degree term life is predictable and budget friendly, which makes it among the most preferred kinds of life insurance policy.

{kind=link}

Latest Posts

Burial Expenses Insurance

Aarp Burial Life Insurance

Final Expense Fund